Cash Loans: Everything Borrowers Should Know About Flexible Lending Options

The Ins and Outs of Loans: Navigating Your Financing Options With Confidence

Maneuvering the complex landscape of loans needs a clear understanding of numerous types and vital terminology. Several people locate themselves overwhelmed by choices such as personal, auto, and pupil loans, as well as crucial ideas like rate of interest prices and APR. A grasp of these basics not only help in assessing economic demands yet likewise improves the loan application experience. Nonetheless, there are considerable elements and typical challenges that consumers should acknowledge prior to proceeding further.

Understanding Various Kinds of Loans

Loans function as necessary monetary tools that deal with various requirements and objectives. Companies and individuals can pick from numerous sorts of loans, each designed to meet specific demands. Individual loans, frequently unsafe, provide borrowers with funds for different personal costs, while car loans allow the acquisition of vehicles with safeguarded funding.

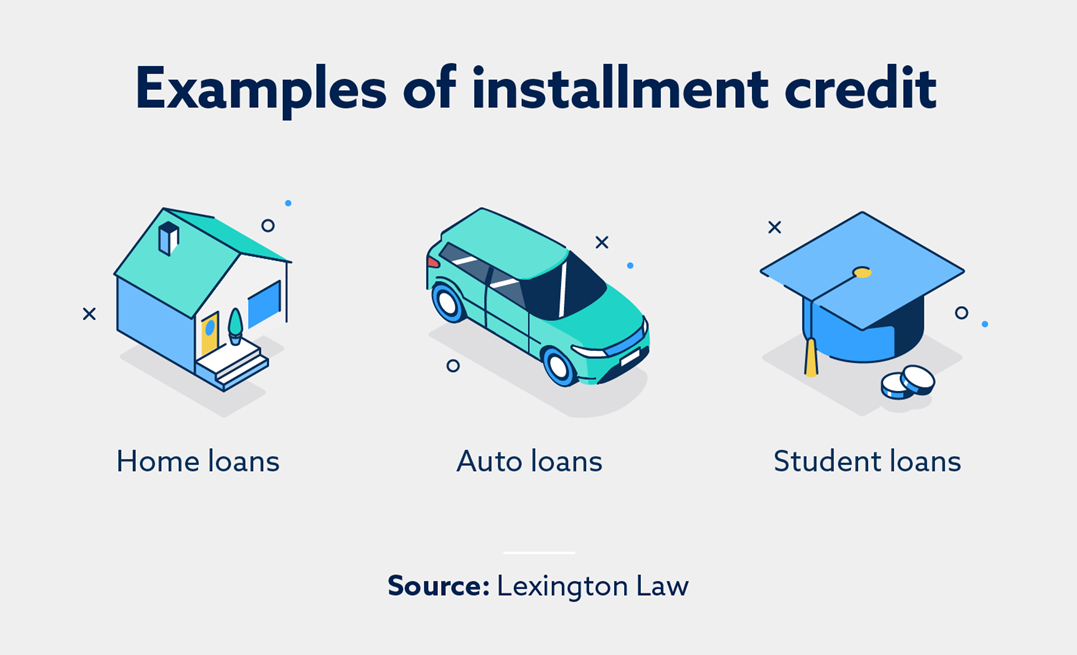

Mortgage, or home mortgages, aid purchasers in obtaining property, commonly entailing lengthy repayment terms and certain rates of interest. Pupil loans, focused on funding education, typically come with lower passion rates and credit options up until after college graduation.

For businesses, industrial loans supply essential resources for growth, tools purchases, or operational expenses. Additionally, payday loans supply fast money remedies for urgent needs, albeit with higher rate of interest prices. Comprehending the different sorts of loans enables debtors to make informed decisions that line up with their monetary goals and conditions.

Secret Terms and Concepts You Need To Know

When navigating loans, comprehending vital terms and concepts is vital. Rate of interest rates play a crucial role in determining the cost of loaning, while various loan kinds deal with different monetary demands. Familiarity with these aspects can encourage people to make informed decisions.

Rate Of Interest Rates Clarified

Just how do rate of interest influence loaning choices? Rates of interest stand for the expense of borrowing money and are an important factor in financial decision-making. A greater rate of interest boosts the overall expense of a loan, making loaning much less appealing, while reduced prices can incentivize customers to take on debt. Lenders usage rates of interest to alleviate risk, reflecting customers' creditworthiness and dominating financial conditions - Payday Loans. Dealt with rates of interest remain consistent throughout the loan term, supplying predictability, whereas variable prices can change, potentially bring about higher settlements with time. Furthermore, understanding the yearly portion rate (APR) is essential, as it includes not simply interest however additionally any type of associated fees, offering a detailed view of borrowing prices

Loan Types Review

Maneuvering the landscape of loan types is essential for debtors seeking one of the most ideal financing choices. Recognizing various loan kinds helps individuals make notified choices. Individual loans are typically unprotected, suitable for consolidating financial obligation or funding individual jobs. Mortgages, on the other hand, are protected loans specifically for purchasing real estate. Auto loans offer a similar purpose, financing automobile acquisitions with the vehicle as security. Organization loans deal with entrepreneurs needing funding for procedures or development. Another choice, student loans, help in covering academic costs, frequently with positive payment terms. Each loan kind offers distinctive terms, rates of interest, and qualification criteria, making it crucial for borrowers to assess their financial requirements and capacities prior to dedicating.

The Loan Application Process Discussed

What steps must one require to successfully browse the loan application process? Individuals should evaluate their monetary requirements and identify the type of loan that aligns with those requirements. Next off, they ought to evaluate their credit record to validate accuracy and identify locations for improvement, as this can impact loan terms.

Following this, debtors have to collect required documentation, consisting of evidence of income, employment history, and economic statements. As soon as prepared, they can approach lending institutions to ask about loan items and passion rates.

After choosing a lender, completing the application properly is crucial, as errors or noninclusions can delay handling.

Last but not least, candidates ought to be all set for prospective follow-up demands from the lender, such as extra documentation or information. By adhering to these steps, people can enhance their chances of a smooth and reliable loan application experience.

Elements That Influence Your Loan Approval

When taking into consideration loan approval, numerous crucial elements come into play. Two of the most significant are the credit report and the debt-to-income proportion, both of which offer lending institutions with understanding into the customer's economic security. Comprehending these aspects can considerably enhance an applicant's possibilities of protecting the preferred financing.

Credit Score Value

A credit score functions as a crucial standard in the loan authorization process, influencing lending institutions' perceptions of a customer's financial dependability. Generally varying from 300 to 850, a higher score indicates a background of liable credit history use, consisting of timely repayments and reduced credit rating application. Various factors contribute to this rating, such as settlement background, length of credit rating, kinds of charge account, and current credit queries. Lenders utilize these scores to examine danger, figuring out loan terms, interest prices, and the probability of default. A strong credit history not only boosts approval chances however can likewise lead to more beneficial loan problems. On the other hand, a low rating may cause greater interest rates or rejection of the loan application completely.

Debt-to-Income Ratio

Many lenders think about the debt-to-income (DTI) proportion a vital facet of the loan authorization procedure. This financial statistics compares a person's monthly financial debt repayments to their gross monthly revenue, supplying insight right into their capability to take care of added debt. A reduced DTI ratio suggests a much healthier financial scenario, making customers much more eye-catching to lenders. Aspects affecting the DTI proportion include housing prices, bank card equilibriums, pupil loans, and various other repeating expenditures. Additionally, modifications in revenue, such as promos or job loss, can significantly influence DTI. Lenders commonly favor a DTI proportion listed below 43%, although this threshold can vary. Managing and comprehending one's DTI can boost the possibilities of protecting positive loan terms and interest rates.

Tips for Handling Your Loan Sensibly

Common Blunders to Stay Clear Of When Taking Out a Loan

In addition, many people rush to approve the initial loan deal without contrasting alternatives. This can result in missed out on possibilities for much better terms or lower rates. Customers ought to also stay clear of taking on loans for unnecessary costs, as this can cause long-term financial obligation troubles. Ultimately, neglecting to analyze their credit rating can impede their capability to safeguard desirable loan terms. By knowing these pitfalls, borrowers can make enlightened choices and navigate the loan process with higher confidence.

Frequently Asked Inquiries

How Can I Improve My Credit Score Prior To Looking For a Loan?

To boost a credit score before obtaining a loan, one should pay costs on time, decrease arrearages, check credit history records for errors, and prevent opening up new charge account. Constant economic practices generate positive outcomes.

What Should I Do if My Loan Application Is Rejected?

Are There Any Type Of Fees Connected With Loan Prepayment?

Funding early repayment charges may use, depending upon the lender and loan kind. Some loans consist of charges for very early settlement, while others do not. It is essential for borrowers to review their loan agreement for specific terms.

Can I Work Out Loan Terms With My Lender?

Yes, borrowers can negotiate loan terms with their lending institutions. Elements like credit report, payment background, and market problems may affect the lender's determination to modify rates of interest, settlement routines, or charges related to the loan.

How Do Rates Of Interest Affect My Loan Repayments With Time?

Rates of interest substantially affect loan payments. Greater rates cause boosted regular monthly payments and complete interest expenses, whereas reduced rates decrease these expenses, eventually impacting the debtor's general financial concern throughout the loan's duration.

Lots of individuals find themselves bewildered by alternatives such as personal, auto, and trainee loans, as well as crucial ideas like rate of interest rates and APR. Rate of interest rates play a crucial duty in figuring out the expense of loaning, while different loan kinds provide to different monetary demands. A greater interest rate boosts the total cost of a loan, making loaning less appealing, while lower rates can incentivize customers to take on financial debt. Fixed passion prices stay constant throughout the loan term, supplying predictability, whereas variable rates can rise and fall, possibly leading to higher settlements over time. Lending prepayment costs might use, depending on the lender and loan type.